THE PAST DEVOURS THE FUTURE: PIKETTY'S CAPITAL

Sander casts a critical eye on Thomas Piketty's Capital in the 21st Century and the debates it provoked

Since its English translation was published, Piketty’s book has made quite a splash on both sides of the Atlantic. The Financial Times called it ‘an extraordinarily important book’ and Esquire Magazine even named it ‘the most important book of the century’ (already!). It climbed to the top spot on Amazon’s bestsellers list, leaving Game of Thrones and How to Win Friends and Influence People in the dust. The highest praise came from left-wing economists like Joseph Stiglitz and Paul Krugman. ‘Conservatives are terrified.’ Krugman wrote in a column in The New York Times, entitled ‘The Piketty Panic’. They are terrified, according to Krugman, because they are unable to negate Piketty’s thesis. He gleefully quoted James Pethokoukis of the American Enterprise Institute who wrote in The National Review that Piketty’s ‘soft Marxism’ must be refuted, otherwise ‘it will spread among the clerisy and reshape the political economic landscape on which all future policy battles will be waged’.

Concerning Piketty’s 'Marxism', there is no need to panic. It doesn’t exist. Of course, by the choice of his title which makes it seem as if he’d written the sequel to Marx’s Capital, he invites the comparison. But in an interview in The New Republic, he rejected any resemblance. He said he had not even read Capital. He stated that, unlike Marx’s, his approach was empirical, not theoretical. That he’s just reporting what the data are telling him. Still, in his introduction, he writes with a hint of sympathy for Marx and declares himself in agreement with what he calls ‘Marx’s principle of infinite accumulation’: the intrinsic compulsion of capital to accumulate for the sake of accumulating.

‘The central contradiction’

You might expect a book that provokes so much talk and controversy to contain some groundbreaking new ideas, but that’s not really the case. Piketty is not the first to show that the inequality of income between the owners of capital and the rest of the population becomes ever larger, or to warn of the social unrest and chaos that this trend could bring. That’s the essence of his thesis. Others have documented the same trend and uttered the same warnings without receiving a bit of the attention Piketty has.

In part, Piketty’s success is due to perfect timing. Inequality of income is a burning theme. And it will become even more so in the next global recession. While unable to provide a solution to the cause of capitalism’s crisis, the capitalist left everywhere points to redistribution of wealth as the way out of our misery. Piketty agrees with this perspective. His own political background is in the capitalist left, specifically the French Socialist Party. He was an advisor to the presidential campaign of Ségolène Royal. As for Royal’s ex, the current president of France, he received Piketty a couple of times in his palace, but judging from his policies he didn’t take his advice.

The book’s success is also due to the fact that it’s well written. Economic jargon and mathematical argumentation are kept to a minimum and there are many interesting literary and historical sidesteps. Furthermore, this ‘monster’ (685 pages, with a large addendum online) is the most extensive study ever undertaken of the history of income inequality in capitalism. Piketty and his many collaborators worked on it for 15 years.

He compares the growth rate of capital with that of the economy in the most developed countries from the 18th century till today. He calls the first ‘r’ and the second ‘g’. His main finding is that r > g is the general tendency. In other words, growing income inequality is baked into the system; it follows from its natural course. Piketty calls this ‘the central contradiction of capitalism’.

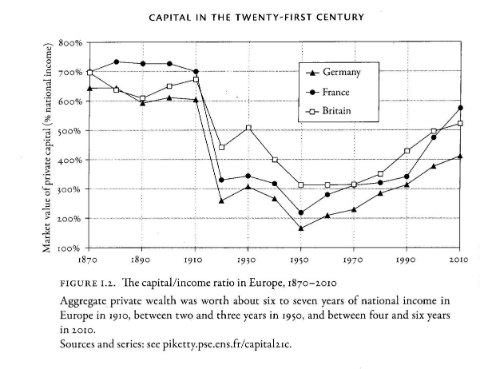

The average yearly growth rate of capital over the entire period hovered around 4-5 percent, while for the economy as a whole (the national income) it was less than 1 percent. Until the ‘industrial revolution’ in the early 19th century, it was even less than 0.1 percent. Then it accelerated. The average yearly growth in the 19th century was 1 to 1.5 percent. But the part that went to the owners of capital grew considerably faster, so that by the end of the century, aggregate private wealth was worth 6 to 7 years of national income (in France, Germany and Britain). A wealth gap equal to that of the Ancien Regime.

But then things changed. From 1914 to 1950 the trend reversed and the gap declined. But the reason was not that the income of those who don’t own capital rose but that capital devalued. The world wars and the depression between them diminished the yield of capital through inflation, outright destruction, and high taxation to finance the wars. During the Second World War it fell almost to zero.

Then followed a period of strong economic growth. Capital grew likewise. For thirty years, both had a yearly growth-rate exceeding 4 percent. It was the only period in which they were in balance, in which r = g. Piketty thinks that the strong growth of ‘les trente glorieuses’ was mainly due to the reconstruction after the war and that it ended when that ended. The growth of the national income declined but the growth of capital did not. Piketty attributes this to fiscal, deregulatory and monetary policy changes spearheaded by Reagan and Thatcher, but also to a shift in the balance of power to the advantage of global capital, resulting from the globalising tendency of the economy and the removal of obstacles to the international mobility of capital. He concludes from his data that a highly developed capitalist country cannot hope to achieve a higher rate of growth than 1 to 1.5 percent (which is more than most of them have today, not to speak of next year). Yet capital continues to grow at a rate of 4 to 5 percent. Hence, the gap widens, approaching the levels from before World War I. Piketty’s data show that 60 percent of the growth of the national income of the US between 1977 and 2007 went to the richest 1 percent of the population. The gap between the growth of capital and of national income in European countries like Britain and France became even wider than in the US. He sees the growing automation as an accelerator of the trend, by reducing the role of living labour in production. More of its yield goes to capital, less to the working population.

The theoretical endpoint of this trend would be that the entire national income goes to capital, which is of course impossible. But already long before that point would be reached, the social fabric of society would be shredded. The possible consequences would be terrifying, writes Piketty. To prevent this disaster, a redistribution of wealth, through a change of fiscal and monetary policies on an international level, is urgently needed.

Headwinds

His position was of course sharply criticised by right-wing ideologues. We can ignore most of them. After all, people who insist capitalism is a 'meritocracy', while it has created a world in which 40 percent of wealth is owned by 1 percent of the population and half the population has an income of less than 2 dollars a day, cannot be taken seriously. Chris Giles of The Financial Times examined Piketty’s data with a magnifying glass. He found some errors and criticised some questionable assumptions. That is not surprising. Piketty analysed a gigantic quantity of data from 20 countries. Some were incomplete and based on different criteria. Their comparison inevitably creates problems. But Giles’ critique does not lead to different conclusions. ‘The most striking fact is how closely The Financial Times’ analysis agrees with Piketty’s’, writes Justin Wolfers in The New York Times. Clive Crook, in a column for Bloomberg News, rejected Piketty’s view that income inequality is ‘the central contradiction of capitalism’. Not the distribution of wealth but its production is the central problem, he insists. He has a point, but for him this just means that 'a rising tide will lift all boats'. But where will this tide be coming from? He doesn’t seem to know either. The one we’re seeing now only lifts the yachts.

The radical ecologist writer Howard Kunstler also thinks that Piketty, by focusing only on the distribution of wealth, ignores the problems facing its creation. For him the central problems are climate change and the exhaustion of fossil fuels. The hope that new technology will make it possible to continue ‘the industrial orgy’ is an illusion. The collapse approaches. Compared with that threat, the income gap seems a minor problem to him. He doesn’t disagree with Piketty’s findings but thinks it’s naïve to assume that the gap can be diminished by political means. ‘Capitalism is like gravity’, he writes. It imposes its laws on the owners of capital, on companies, on the state. It resists all attempts to try to correct its fundamental mechanisms.

To some extent, Piketty agrees. He concludes from his data that, in regard to the income gap, it matters little which government is in power: Democrats or Republicans, Labour Parties or Conservatives; it made no difference regarding the general trend of the period. Governments can do useful things according to Piketty but they are essentially powerless to stop the growth of the income gap. There are only two ways to do it, he points out: increasing the growth of the national income or reducing the part of it that goes to capital. He thinks the first road is limited, since, as mentioned earlier, he came to the conclusion that highly developed countries can grow at a no higher rate than 1.5 percent a year. But the second is limited too. Thomas Edsall writes in The New York Times: ‘Piketty’s analysis articulates what many people on the Democratic left feel intuitively, that a domestic tax, spending and regulatory agenda is ineffective in the face of the power of globalised capital to grind down wages and benefits.’

Edsall remarks that this part of Piketty’s theory is less appreciated by the left. He quotes Robert Kuttner, editor of The American Prospect, who thinks Piketty’s book fosters ‘passivity and acceptance’ and the economist Dean Baker who sneers that ‘a big part of the book’s appeal is that it allows people to say capitalism is awful but there is nothing that we can do about it’.

A world tax

Piketty thinks something can be done about it, but only on a global level. Only through an international tax on great fortunes can the growth of global inequality be reined in. But what we see in reality is the opposite trend: increasing competition between states to lure capital with fiscal advantages. Despite their rhetoric, they are not even able to agree on joint measures against 'tax havens', although these obviously diminish their income, because these havens have become essential parts of capitalism’s functioning. Not surprisingly, most of his critics think Piketty’s proposal is utopian. To which Piketty replies that in the early 20th century the idea of a progressive income tax was considered utopian as well. But then came the world war, which made it a necessity and today it is accepted as normal.

It’s interesting that war plays a large part in Piketty’s analysis. As it should, since it played a large part in the period he examines. He shows its consequences on growth, on income, on the yield of capital. But he sees war as an external factor impacting the economy, not as one that has itself economic roots. Neither does he sees a causal relation between economic growth and the yield of capital. ‘Strictly speaking, capital and economic growth have nothing to do with each other’, he claims. He asserts that it was not economic growth but the increasing valuation of land that was the main source of the growth of capital in the 19th century, and that the high yield of capital today can’t be explained by economic growth either. He emphasises the complexity; the role of political, cultural and other factors. We can agree on the complexity but by uncoupling the yield of capital from economic growth, Piketty ignores the question where capitalist wealth is coming from. He doesn’t ask, for instance, where the purchasing power that drove up the price of land in the 19th century came from nor why the demand for it rose. For him, wealth can grow by itself.

What is capital?

It is therefore not surprising that several critics charge that Piketty doesn’t understand what capital is. His definition is at once restrictive (he looks only at what is privately owned) and very broad. All exchangeable forms of possessions (land, real estate, companies, technology, financial assets, etc.) fall under it. Tyler Cowen reproaches Piketty in Foreign Affairs in that he sees capital as ‘a growing, homogeneous blob’, ignoring the many differences between its components. Yet in a sense, capital is an homogeneous blob. It comes in many forms but it can instantly change from one form to another. The whole ‘blob’ is subject to the same compulsion to grow, on penalty of devaluation.

More pertinent is the critique of the Keynesian economists James Galbraith and Brad De Long, who claim that Piketty confuses capital and wealth. He does not distinguish between productive capital and capital that just sits there and grows in value simply because it represents a share of the total purchasing power: what can be bought with it increases in value because the value of total production increases. Piketty’s Marxist critics sharpen that point. ‘Capital is a process not a thing. It is a process of circulation in which money is used to make more money’, emphasises David Harvey. ‘The rate of return on capital depends crucially on the rate of growth because capital is valued by way of that which it produces and not by what went into its production.’ Esteban Maito tried to isolate the course of productive capital in Piketty’s data. He asserts that this correction makes the stable high yield of capital disappear. Instead, Maito claims, the data confirm Marx’s law of the tendential fall of the rate of profit . According to this theory, the declining role of living labour in production implies a declining production of surplus value, and hence of profit, leading to crisis, and devaluation of capital, which cheapen production costs, reconnect supply and demand and thereby set a new accumulation cycle in motion, until crisis strikes again.

What is certain is that Piketty’s data confirm that crisis and war devalue capital and that this devaluation creates room for new growth. But that’s no longer true in the post-WW II period. Piketty shows that neither the crisis in the 1970s nor the one that broke in 2008 caused a general devaluation of capital. They led to a decline of economic growth but not of the growth of capital (as defined by Piketty). There was no correction because capitalism resisted it. New capital was massively created to prop up the value of the existing capital; to prevent, or at least postpone, its devaluation.

And on it goes. The Fed (American central bank) alone has since 2008 created, out of nothing, 3.7 trillion dollars. And the central banks of the EU, Japan and China have created trillions more. The Fed recently stopped its quantitative easing program but keeps interest rates close to zero, which also creates money for the rich. Meanwhile, Japan announced it will expand its quantitative easing. None of this new capital results from production and neither is it invested in production. Its purpose is, by and large, to give capital a greater share of the total purchasing power in order to keep the collective belief in it alive.

It’s fictitious capital, and its fictitious nature would become apparent in rampant inflation if all that new purchasing power were actually used. But the larger part of it isn’t; it remains in the form of money or financial assets. The money creation orgy organises a redistribution of wealth which accomplishes two goals: it maintains capital’s yield and sterilises it against the ill effects of excess money by locking it up in the fortunes of the rich and the coffers of the central banks.

Piketty does not analyze the causes of the crisis of 2008. But he brings ample evidence to the thesis that financial overaccumulation played a major role. An ever larger part of capital is neither invested in production nor consumed nor engaged through the credit market in the future creation of value, yet demands a growing share of the total purchasing power. The more the value of capital is being inflated, the heavier its claims on the real economy become. The longer capital grows in excess of the economy, the more the latter sinks into debt. Or as Piketty puts it: ‘The past devours the future.’ This little sentence is quoted by Crook as an example of the incomprehensible language which in his opinion Piketty sometimes falls into. Yet the fact that Crook finds it incomprehensible says more about him than about Piketty. The phrase is a perfect summary of the predicament the world is in.

And yet, Piketty does not distinguish fictitious and non-fictitious capital. He looks at this enormous mass of unused capital and sees no reason why it couldn’t be employed for the general good. ‘When you have so much private capital and wealth at your disposition, it seems stupid not to use this possibility’, he says.

He wants to force capitalism to grow. But if this increased growth would be sufficiently profitable, capital would flow to it by itself, it wouldn’t need to be forced. So he wants capitalists to accept a lower rate of profit or no profit at all. Also, he wants them to accept higher taxes. And to set fiscal competition aside. To come together for the common good. Good luck with that.

Piketty is indeed utopian because of the irreconcilable contradiction between the framework he wants to keep (‘I love capitalism’, he declared in an interview on CNBC) and the goal he wants to achieve. About the Pikettys of his time Marx wrote: ‘What divides these gentlemen from the bourgeois apologist is, on the one side, their sensibility to the contradictions of the system; on the other, the utopian inability to grasp the necessary difference between the real and the ideal form of bourgeois society, which is the cause of their desire to undertake the superfluous business of realising the ideal expression again’. A capitalism with a human face is what they want but a capitalism with a human mask is what they actually contribute to.

A blurb on the back cover of Piketty’s book quotes Dani Rodrik of the ‘Institute for Advanced Study’: ‘Whether you agree or not on the solution, the book presents a stark challenge to those who would like to save capitalism from itself’. Piketty's goal is indeed to save capitalism from itself. But that is neither possible nor desirable.

Info:

Capital in the Twenty-First Century, Thomas Piketty, Harvard University Press, 2014

Sander uses this pseudonym for his more important articles. He fears that otherwise, he might not get any more work as a journalist. He lives in New York and is a collaborator of the pro-revolutionary review Internationalist Perspective:

http://internationalist-perspective.org/

Mute Books Orders

For Mute Books distribution contact Anagram Books

contact@anagrambooks.com

For online purchases visit anagrambooks.com

Related Content

Proud to be Flesh: A Mute Magazine Anthology of Cultural Politics after the Net